The folderK2 Integrityputs the Lebanese banks in front of a choice they have been pushing for years: to comply with stricter international requirements or to remain in growing financial isolation. Mandated by the Bank of Lebanon to help the country emerge from the FATF’s grey list, the US firm intervenes in a banking system already discredited by the 2019 crisis, blocked deposits, dollarization in cash and the distrust of foreign correspondents. Officially, this is technical support against money laundering, fraud and terrorist financing. In the banking community, the case is also seen as a direct US pressure on financial flows, transfers and grey areas of the Lebanese economy.

The issue is not just regulatory. It affects Lebanon’s financial sovereignty. Banks accept the principle of compliance because they know that a country under enhanced supervision pays more for its transactions and loses access to normal banking relations. But they fear the cost of the scheme, the exact role of K2 Integrity, possible access to sensitive data and the impression that part of the supervision of the financial system would be entrusted to a foreign actor close to the US sanctions channels. Lebanon wants to get out of the grey list. He must avoid giving the feeling that he entrusts his bank keys to Washington.

The grey list as accelerator

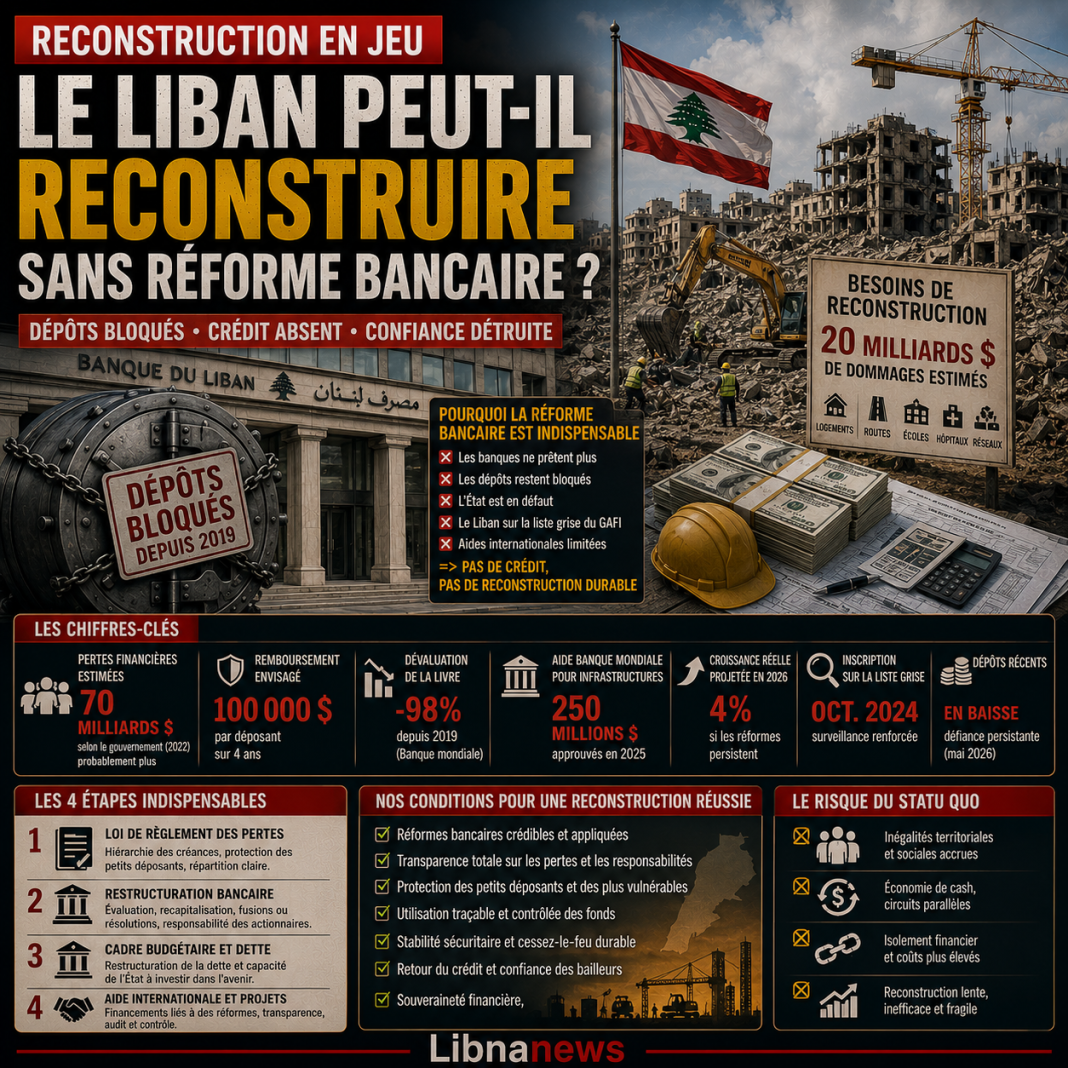

Lebanon entered the FATF grey list in October 2024. This listing, officially referred to as enhanced monitoring, does not correspond to a blacklist. It does not mean that Lebanese transactions must be blocked. She noted, however, that the country had strategic weaknesses in combating money laundering, terrorist financing and proliferation financing. For a country whose banks have already lost the confidence of a large part of depositors, the reputational impact is heavy.

Suivez les principaux indicateurs économiques en temps réel.

The FATF Action Plan covers several areas. Lebanon must better assess the risks of money laundering and terrorist financing. It should strengthen mutual legal assistance, asset recovery, transparency of beneficial owners, financial investigations, prosecution, seizure of illegal cross-border movements and the prompt application of targeted financial sanctions. It must also monitor organisations at risk without discouraging the legitimate activity of associations. This programme is extensive. It is not just about banks. It affects foreign exchange offices, transfer companies, real estate, non-financial professions, NGOs and justice.

The stakes are all the more important as Lebanon has been operating since the crisis on a largely cash-based economy. Households avoid banks. Companies settle part of their cash transactions. Diaspora transfers support consumption. Informal circuits have gained more weight. This has enabled the economy to survive. It has also increased the risk of untraceable flows. The foreign partners therefore ask Lebanon to reintegrate financial movements into controlled circuits, without breaking the flows that allow families to live.

K2 Integrity, technical tool or political signal?

In this context, the Bank of Lebanon signed an agreement with K2 Integrity in July 2025. The U.S. firm specializes in risk management, financial investigations, compliance, anti-money laundering and advice to jurisdictions under regulatory pressure. According to available information, its mandate is to support the Bank of Lebanon in the adoption and implementation of measures to strengthen the national machinery for combating illicit activities. The official message is clear: Lebanon wants to show the FATF and its partners that it is acting.

The use of an American firm is a practical logic. The United States plays a central role in the global compliance architecture. The dollar remains the main currency for international settlement. The corresponding US and European banks largely determine Lebanon’s access to the global financial system. A mechanism deemed credible in Washington can therefore help Beirut to reassure markets. For the Bank of Lebanon, the support of a well-known compliance firm can also speed up the production of procedures, reports, training and action plans.

But this choice raises questions. K2 Integrity has or has counted profiles from the US financial security, treasury, investigation and sanctions universe. For some Lebanese officials, this is an asset. For others, it is a risk. Lebanon is already under US pressure to finance Hezbollah, foreign exchange offices, transfer companies and Iran-related networks. In this climate, the mandate of an American firm cannot be seen as neutral by the whole sector. Compliance then becomes a geopolitical issue.

Lebanese banks: the cost and fear of control

The unease of banks begins with the scope of the mandate. A technical advisory role does not pose the same problem as a role of direct or indirect supervision of transfers. While K2 Integrity is limited to assisting the Bank of Lebanon in drafting procedures, identifying gaps and training teams, the issue remains manageable. If the firm intervenes in the monitoring of transactions, in the definition of alerts, in access to certain data or in the evaluation of banks, the sensitivity increases sharply.

Banking institutions also fear compliance costs. Since 2019, they have been operating in a deeply weakened sector. The balance sheets remain subject to losses. Old deposits remain blocked. The normal credit did not resume. Revenues come primarily from fees, services and accounts. Adding filtering, reporting, audit, training and IT upgrade requirements is a real burden. Large banks can absorb some of these costs. Smaller firms may be subject to additional pressure at a time when bank restructuring remains incomplete.

This concern should not mask a responsibility. Lebanese banks have long benefited from a model based on deposits, high yields and the relationship with the State. The crisis revealed the flaws of this system. Compliance cannot be presented only as an external constraint. It is also a condition for regaining a minimum of credibility. Establishments that refuse any enhanced control fuel mistrust. Those who accept an unsecured upgrade to data feed another fear: that of outsourcing sovereignty.

Financial data, sovereignty issue

The file raises a specific question: who controls Lebanese financial data? Bank information, transfers, beneficial owners and compliance alerts are not mere administrative files. They can reveal business relationships, family flows, political networks, commercial activities and judicial vulnerabilities. In a country exposed to US sanctions, access to these data becomes strategic. Banks therefore ask for guarantees of confidentiality, location of information, persons authorised to consult it and use it.

The Bank of Lebanon must clarify this point. It cannot ask banks to cooperate while leaving an ambiguity about the real role of the firm. The rules must be written. The terms of reference should specify whether K2 Integrity advises, audits, recommends, supervises or receives data. He must say what information is coming out of the banks, in what format, with what protections and under what Lebanese authority. It shall also provide for liability for leakage, misuse or unauthorized transmission. Without these guarantees, compliance will be seen as guardianship.

Sovereignty should not, however, be used as a pretext for refusing transparency. Bank secrecy has long protected against practices that have adversely affected the public interest. The partial lifting of this secret, voted in the context of financial reforms, marks a necessary break. It should enable the Lebanese authorities, the judiciary, the tax administration and the supervisory bodies to work better. But sovereignty requires that such control be institutionalized. It must go through the Bank of Lebanon, the Special Investigation Commission, justice and the competent authorities, not through opaque channels.

Washington, Hezbollah and Transfers

The US pressure has a clear objective: to prevent the Lebanese system from serving as a funding channel for sanctioned networks. In particular, Washington targets Hezbollah, its financial allies, certain foreign exchange offices, transfer companies and Iran-related circuits. US officials believe that the cash economy and weaknesses of Lebanese control can help circumvent sanctions. This position is constant. It was reinforced with the regional war and with the negotiations on the Iran-USA agreement.

For Lebanese banks, this pressure creates a dilemma. Cooperating with U.S. requirements can preserve corresponding relationships and avoid secondary sanctions. But cooperation without a clear Lebanese framework can give the impression that banks are responding first to Washington. Resisting can satisfy a sovereignist discourse, but expose the country to more financial isolation. In practice, banks are likely to choose prudence. They will apply requests for access to currencies and international transactions while seeking to limit their political liability.

The government cannot remain a spectator. Banking compliance is not a subject reserved for technicians. It covers diaspora transfers, imports, exports, NGOs, traders, hospitals, universities and households. Poorly calibrated hardening can slow down legitimate flows and further encourage cash. Too little supervision can keep Lebanon on the grey list and threaten banking relations. The adjustment must therefore be national, transparent and proportionate.

Quantified compliance priorities

The output of the grey list requires a complete architecture. It will not be obtained by contract with a foreign firm, even if deemed. FATF requires results, not just consultants. It wants to see investigations, prosecutions, judicial decisions, effective sanctions, greater corporate transparency, oversight of non-financial professions and a real capacity to seize illicit movements. Lebanon must therefore work together with the Bank of Lebanon, the Special Investigation Commission, the Ministry of Finance, justice, customs, security forces and supervisory authorities.

| Indicator or requirement | Data or issues | Impact on banks |

|---|---|---|

| Inclusion of Lebanon in the grey list | October 2024 | Enhanced surveillance and reputational risk |

| FATF Action Plan | Ten main axes | Pressure on banks, justice, beneficial owners and targeted sanctions |

| Bank of Lebanon-K2 Agreement Integrity | July 2025 | Technical support, but debate on the real perimeter |

| Cash saving | High share since 2019 | Increased risks of untraceable flows |

| Diaspora transfers | Billions of dollars a year | Need to control without discouraging legitimate flows |

| Banking reform | Still unfinished | Compliance goes ahead without a clean balance sheet |

The difficulty is that compliance progresses faster than restructuring. Banks are called upon to meet standards, while their main problem is not solved: who is responsible for the losses? As long as the old deposits remain blocked, as long as the balance sheets are not cleared, as long as the shareholders, the State, the Bank of Lebanon and the depositors do not know their share of the losses, confidence will remain low. Compliance can prevent international degradation. It will not restore credit alone.

Complying without resolving the banking crisis?

This lag is fuelling bank reluctance. Establishments can claim that they bear a compliance cost in a system where the state has not yet resolved the crisis. They may also be concerned that enhanced controls may reveal past practices, disputed transfers or responsibilities in deposit management. Compliance is not just about the future. She can bring back the past. This is one of the reasons why resistance is strong.

The IMF, donors and partners in Lebanon do not separate these issues. In their view, exiting the crisis requires a package: banking reform, effective lifting of bank secrecy for the competent authorities, recapitalisation or resolution of banks, capital control, anti-money laundering, financial justice and protection of small depositors. Lebanon has often advanced in pieces. It adopts a law, signs a contract, announces a commission, and then lets implementation get lost. The K2 Integrity file will be judged on the application, not on the advertisement.

Banks should therefore ask for a clear framework rather than refuse the principle. They may require a strict separation between technical advice and access to data. They may request that any information be submitted by the competent Lebanese authorities. They may require reasonable deadlines, proportionate standards and protection against political usage. But they cannot ask for a return to an opacity that contributed to the rupture with applicants and with foreign partners.

Minimum transparency to avoid guardianship

The main risk is twofold. The first would be to transform K2 Integrity into a symbol of US supervision over Lebanese banks. This would fuel political distrust, strengthen actors hostile to compliance and complicate cooperation. The second would be to use the fear of guardianship to block any reform. This would keep Lebanon on the grey list, increase transaction costs and further isolate banks. Between these two impasses, there is a narrower way: to accept expertise, but to regulate its use legally.

This means publishing the outline of the mandate. The public does not need access to sensitive operational details. However, he must know what the firm is doing and what it is not doing. He must know whether the individual data are protected. He should know which Lebanese authority oversees the scheme. He needs to know how banks will be evaluated. He should also know how the results will be forwarded to the FATF. In a country where confidence has been destroyed by secrecy, minimum transparency becomes a condition of stability.

Parliament should also play its role. Compliance should not be managed solely through circulars, contracts and technical meetings. It commits financial sovereignty, data protection, the relationship with the United States, the removal of the grey list and the restructuring of the sector. Parliamentary committees may hear the Bank of Lebanon, the Bank Association, the Special Investigation Commission and the relevant ministries. They may request guarantees without exposing sensitive information. Democratic control should not be confused with obstruction.

The real choice: control or isolation

Lebanon will not be able to return to a normal banking relationship without credible compliance. Foreign correspondents will not return out of sentimental confidence. Transfers will not be facilitated by sovereignist discourse. Investors will not only look at promises of reform. They will verify procedures, sanctions, controls, judicial decisions and the State’s ability to enforce its rules. The grey list acts as a permanent reminder: the Lebanese problem is institutional as well as banking.

At the same time, compliance should not become a delegation of sovereignty. A weakened state can seek help from a foreign firm. It must not abandon the definition of national priorities. The Bank of Lebanon must use K2 Integrity as a tool, not as a substitute. Banks must accept stronger control, not frameworkless supervision. The United States authorities may demand guarantees against illicit financing, not substitute for Lebanese institutions. The border is fine. It will decide on the acceptability of the device.

The K2 Integrity file thus reveals the central dilemma of financial Lebanon. Compliance is essential. Staying alone would be even more expensive. But to comply without sovereignty, transparency and complete banking reform would only replace one crisis with another. Lebanese banks no longer have the luxury of choosing opacity. The Lebanese state no longer has the luxury of choosing improvisation. The next steps will say whether compliance becomes a path to financial reintegration, or a new ground of mistrust between banks, Washington, the Bank of Lebanon and depositors.