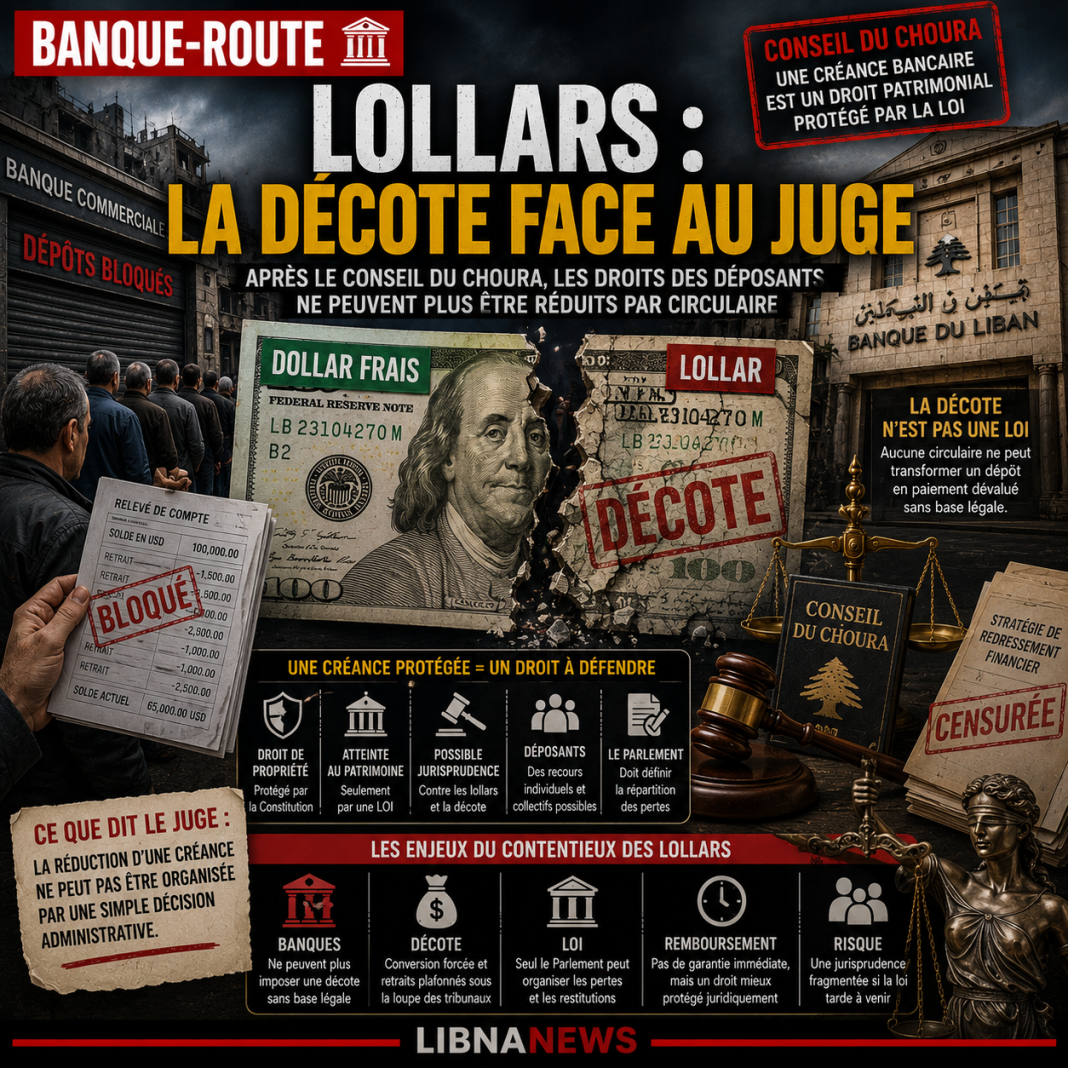

The debate on Lebanese bank deposits is no longer just a matter of financial technology. It became a test of legality. Since the Choura Council’s decision cancelling part of the government’s recovery strategy, the executive can no longer treat depositors’ claims, Bank of Lebanon’s liabilities and bank losses as mere accounting variables. The crisis imposes burden-sharing. But this division must now go through the law, respect the right to property and define a clear hierarchy of responsibilities.

This constraint changes the position of all actors. The government must transform a political choice into a legislative architecture. The Bank of Lebanon, led by Karim Suaid since 2025, must defend monetary stability without becoming the window for the defeat of commercial banks. Banking institutions seek to limit their contribution on behalf of investments made with the central bank and government debt. The applicants claim a simple principle: their assets cannot be amputated by an administrative decision, without a legal basis, without parliamentary scrutiny and without guarantees of restitution.

This sequence puts Lebanon before a hard equation. We must recognize losses, protect small accounts, restructure insolvent banks and avoid a new monetary creation that would destroy the stability of the pound. But it is also necessary to take account of a judicial decision that closes the way for shortcuts. The executive may propose. He can arbitrate. It can negotiate with the International Monetary Fund and donors. It can no longer erase rights by circular, ministerial plan or simple balance sheet writing.

Suivez les principaux indicateurs économiques en temps réel.

Choura Council sets a political limit

The decision of the Choura Council moved the centre of gravity of the case. For several years, the authorities operated in a grey area. Banks have imposed restrictions without formal capital control laws. The Bank of Lebanon has multiplied the circulars to organize partial withdrawals. The State allowed losses to accumulate without defining an effective strategy. This management by exception has produced a normality of crisis. The administrative judge recalled that this normality cannot replace the law.

The constitutional scope of the case lies first of all in the right of ownership. A bank deposit is a legal claim against a bank. It is not physically stored in a safe. But this debt remains a property asset. It goes into the protection of private property. Reducing, converting, spreading or subordinating it therefore requires an explicit legal basis. The more the measure affects the actual value of the deposit, the stronger the requirement of legality.

The Choura Council did not resolve the entire crisis. He did not say that all deposits could be repaid in full and immediately. It did not remove the losses. Rather, it has set an institutional limit. A government cannot, through an administrative strategy, cancel a large part of the Bank of Lebanon’s commitments to banks and then let this cancellation affect depositors mechanically. Such an operation modifies property rights. It affects the balance of contracts. It commits Parliament.

This limit is essential. It prevents the executive from turning a systemic bankruptcy into a unilateral decision. It requires the appointment of responsibilities. It also forces the authorities to choose between several legal paths. The first is the recognition of a public debt to the Bank of Lebanon for losses attributable to the State. The second is to impose a real contribution on bank shareholders and then on holders of subordinated instruments. The third is to organise a differentiated return of deposits, with priority protection for small accounts. The fourth is to deal separately with illicit deposits, excessive interest and transactions related to artificial conversions.

The decision of the administrative judge therefore does not only protect banks, although the Association of Banks used it in its argument. It also protects a procedural principle. Property infringement cannot be concealed in a reorganization plan. It must be debated, voted, framed and controlled. This is the point that now makes any attempt to circumvent by the Bank of Lebanon or the government more difficult.

Deposits at the heart of the passage required by law

Parliament thus becomes the compulsory passage. The « financial hole » law, or Gap Law, responds to this need. It seeks to organize the distribution of losses between the State, the Bank of Lebanon, commercial banks and depositors. It promises priority protection for deposits up to $100,000, with extended repayment terms. For higher amounts, it envisages longer mechanisms, including instruments backed by assets or future flows. This logic aims to avoid an immediate shock on public finances and money supply.

But the draft raises a substantive issue. Can a law legalize a loss without ensuring credible reparation? The answer will depend on its final content. A law that names losses, establishes categories, imposes audits and provides for a hierarchy of sacrifices can be defended as an act of stabilization. A law that transfers most of the cost to depositors, without the effective contribution of banks and without the responsibility of the State, risks being perceived as disguised confiscation.

The constitutional issue is not limited to property rights. It also concerns the separation of powers. The government can negotiate with the IMF. It can prepare texts. He can defend a fiscal trajectory. But the liquidation of part of bank claims requires a vote. Parliament must take the choice publicly. This requirement is politically demanding. It obliges MEPs to decide on the hierarchy of losses, not to let the Bank of Lebanon deal with the social consequences alone.

Bank of Lebanon under Karim Suaid

The Bank of Lebanon is at the centre of this architecture. Under Karim Suaid, she must arbitrate between three imperatives. The first is monetary: avoid a new spiral of devaluation. The second is banking: restoring a minimum of confidence in payments and balance sheets. The third is legal: do not make decisions on it that are the responsibility of the legislator. The Governor may supervise, monitor, impose prudential standards and provide data. He cannot decide alone who loses, who recovers and at what rate.

This distinction is decisive. The Bank of Lebanon has long been both a central bank, a state financier, a bank regulator, an exchange rate manager and an actor in quasi-budgetary policies. This concentration has contributed to blurring responsibilities. The Souaid period should mark a break. The central bank must return to a limited role: monetary stability, supervision, balance sheet transparency and banking discipline. If it becomes the main payer of the crisis, it will reproduce the scheme that led to the collapse.

The Bank of Lebanon’s margin of manoeuvre remains real. It may require banks to review the quality of assets. It can impose recapitalization plans. It can distinguish viable establishments from those that need to be merged, liquidated or resolved. It can also strengthen provisioning obligations and prevent dividend distribution as long as deposits remain blocked. These instruments are within its regulatory mandate. They do not require her to assume private losses.

On the other hand, its margin becomes narrow when it comes to financing the refund. If the Bank of Lebanon issues financial instruments to repay large depositors, it must ensure that these securities are based on real assets, identifiable flows and verifiable governance. Otherwise, they will become new « lollars »: promises denominated in dollars, but valued at a fraction of their amount. Such a solution would stabilize the balance sheets on paper. It would prolong mistrust in the real economy.

The risk of a BDL appears to banks

The main risk is to make BDL a screen. Commercial banks could argue that their deposits with the central bank constitute claims on a public institution. They could then limit their own contribution, explaining that the loss is first of all that of the State and the BDL. This reading contains some legal truth. Bank investments with BDL cannot be erased without a legal basis. But it is not enough to exempt banks from their management choices, excessive concentration of sovereign risk and unequal treatment of depositors after 2019.

The hierarchy of losses must therefore be explicit. In an orderly bank restructuring, shareholders absorb losses first. Wrongful leaders must be held accountable for their actions when violations are established. Large creditors and holders of instruments similar to capital may then be solicited. Ordinary depositors should be protected as much as possible, with a clear priority for small accounts. The State intervenes for its responsibility, but without resorting to a monetary issue that would ruin the value of the repayments.

The figures available give the measure of difficulty. The financial deficit was estimated at over $70 billion in the first formal assessments. Commercial bank deposits with the Bank of Lebanon still represented tens of billions of dollars in recent data. The projects discussed refer to deposit protection of up to $100,000, with repayment spread, while large deposits would be treated with long-term instruments. These parameters show that the problem is not just to recognize a right. It is to make this right executable.

Table of economic and legal benchmarks

| Benchmark | Scope for the crisis |

|---|---|

| Over $70 billion in estimated losses | Order of magnitude of the financial hole to be distributed |

| $100,000 threshold per depositor | Priority for small and medium-sized accounts |

| Refund spread over several years | Need to avoid immediate impact on reservations |

| Long-term instruments for large deposits | Risk of liquid securities if assets are uncertain |

| Decision of the Choura Council | Prohibition of circumvention by administrative decision |

These benchmarks show a double constraint. Lebanon cannot promise an instant repayment that its banks and its State cannot finance. Nor can it transform the immediate impossibility into the cancellation of duties. The law must therefore organize a long time, without concealing the actual loss. It must also say who guarantees future instruments, who values them and who bears the risk if the assets advertised do not generate the expected revenues.

Monetary stability as a red line

Monetary stability imposes another constraint. Since the end of the hyperinstability of the pound, the Bank of Lebanon has sought to avoid massive financing in local currency and to limit disorderly interventions. This stabilization remains fragile. It depends on reserves, budgetary discipline, foreign exchange flows and confidence. A poorly funded restitution plan could revive the demand for dollars, exacerbate devaluation expectations and destroy the desired effect. Reimbursing depositors with a weakened currency would mean organizing an inflation loss.

The challenge therefore lies in the order of reforms. Lebanon cannot restore confidence without making deposits partially accessible. But it cannot make deposits accessible without restructuring banks, clarifying losses and preventing further devaluation. It’s a closed circle. In order to open up, a credible sequence is needed: loss law, independent audits, classification of banks, recapitalisation or resolution, return schedule, strict control of monetary creation and gradual reactivation of credit.

The issue of illicit deposits should also be treated with caution. Recent projects provide for a distinction between legitimate deposits and fraudulent funds, excessive interests or privileged transactions during the crisis. The principle seems right. But its implementation requires sound procedures. Combating abuse should not become an arbitrary tool for reducing claims without evidence. Protection of the ordinary applicant also implies protection against blurred categories.

Commercial banks face an alternative. Either they accept deep restructuring, with losses for shareholders, recapitalisation and change in governance. Either they defend nominal survival that keeps depositors captive and the economy without credit. The second option prolongs the crisis. It allows institutions to retain their sign, but it prevents the banking system from fulfilling its function. A bank that does not lend, repay and finance the economy is no longer an intermediary. It becomes a blocking structure.

For Karim Souaid, the issue is institutional. Its credibility will not depend solely on the exchange rate. It will depend on its ability to prevent opaque socialization of losses. A strong BDL is not a BDL that absorbs everything. It is a BDL that imposes rules, publishes reliable figures, resists banking pressures and refuses solutions that make up losses in future assets. Monetary stability cannot serve as an argument to freeze duties indefinitely. It must be the framework for an orderly return.

The government, for its part, can no longer take refuge behind the technicality of the case. The decision of the Choura Council recalled that the law even governs systemic crises. Parliament will have to say what the state’s share is, what the banks’ share is, what the share can be spread out and what guarantees the depositors can protect. He will also have to explain how he avoids two symmetrical injustices: to make taxpayers pay alone to save the banks, or to make depositors pay alone to save the state.

The economic picture is therefore less that of a simple accounting split than of a legal pact. Losses exist. Rights also exist. The law must organize their meeting. It cannot deny the losses, as it would maintain a fictional balance sheet. It cannot deny rights, because it would destroy legality and trust. Between these two limits, the Bank of Lebanon has a regulatory space, not a white-seing.

Lebanon thus faces a specific choice. It can pass a law that covers losses, protects deposits to the extent possible and imposes real discipline on banks. Or it can adopt a text that moves the numbers without changing responsibilities. The first route would be costly, slow and politically conflicting. The second would be easier to vote, but it could be challenged, ineffective and destructive for trust. The decision of the Choura Council reduced the space of the false likes. It now obliges the executive, the Bank of Lebanon and commercial banks to act in a context where the financial crisis does not suspend the law.